The 10x Research May Survey Called It: Long HYPE, Short ETH Returned 74%

Before the Consensus Catches Up

Get your tickets for Bitcoin Asia Conference, Aug 27-28, in Hong Kong.

About the Survey

Each month, 10x Research surveys its subscriber base, active traders, and sophisticated crypto investors to capture real-time sentiment, positioning, and forward expectations across Bitcoin, altcoins, and related asset classes. The May 2026 edition covered ten questions spanning near-term price outlook, year-end targets, allocation behavior, altcoin preferences, catalysts, risks, and relative performance expectations versus gold, equities, and crypto stocks. The results offer a rare ground-level view of how informed market participants are positioned.

Please find below the June Survey with our 12 question survey capturing sentiment, positioning, views and expectations. We will prepare a downloadable pdf with all the charts, interpretations, and survey results.

The 10x Research May Survey Called It: Long HYPE, Short ETH Returned 74%

Participate in the June Survey

Each month, this survey tracks how subscriber conviction evolves alongside market conditions. Click here to participate in the June survey.

Survey Sentiment From the May 10x Research Subscriber Survey

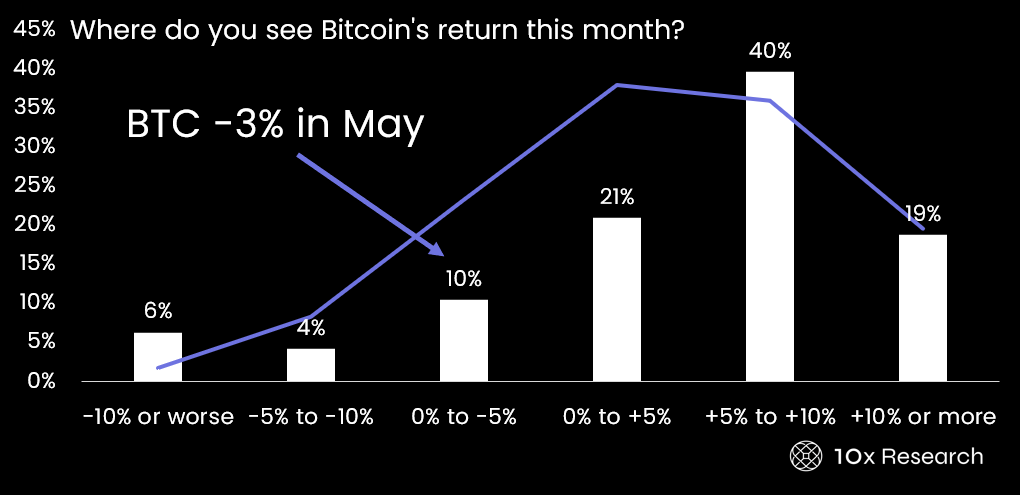

The May survey provided a meaningful read on subscriber positioning. Bitcoin sentiment leaned constructively bullish: 41% expected a +5% to +10% gain for the month, 20% anticipated +10% or more, and only 10% anticipated losses. On the year-end view, 60% see Bitcoin settling between $80k and $120k by December 2026, with just 8% holding above-$150k convictions. Allocation behavior confirmed the tilt, 50% of respondents had either slightly or significantly increased Bitcoin exposure over the prior two months, while only 14% had reduced it.

May Survey Expectations vs. Bitcoin’s actual performance

Overall sentiment was bullish-leaning: 44% bullish or strongly bullish against 28% bearish or strongly bearish. HYPE was the clear altcoin conviction trade, 40% named it most likely to outperform Bitcoin, while ETH led underperform expectations at 35%, followed by SOL at 27%.

On catalysts, (Micro)Strategy buying ranked first at 29%, ahead of regulatory clarity at 19% and Fed rate cuts/liquidity at 16%. The risk picture was unambiguous: macro risk dominated, accounting for 74% of responses and overwhelming every other concern. In the cross-asset comparison, 42% expected Bitcoin to outperform Gold, and 20% expected it to outperform the S&P 500. On crypto equities, subscribers were divided, 25% expected BTC to underperform MSTR specifically, while 25% saw rough parity.

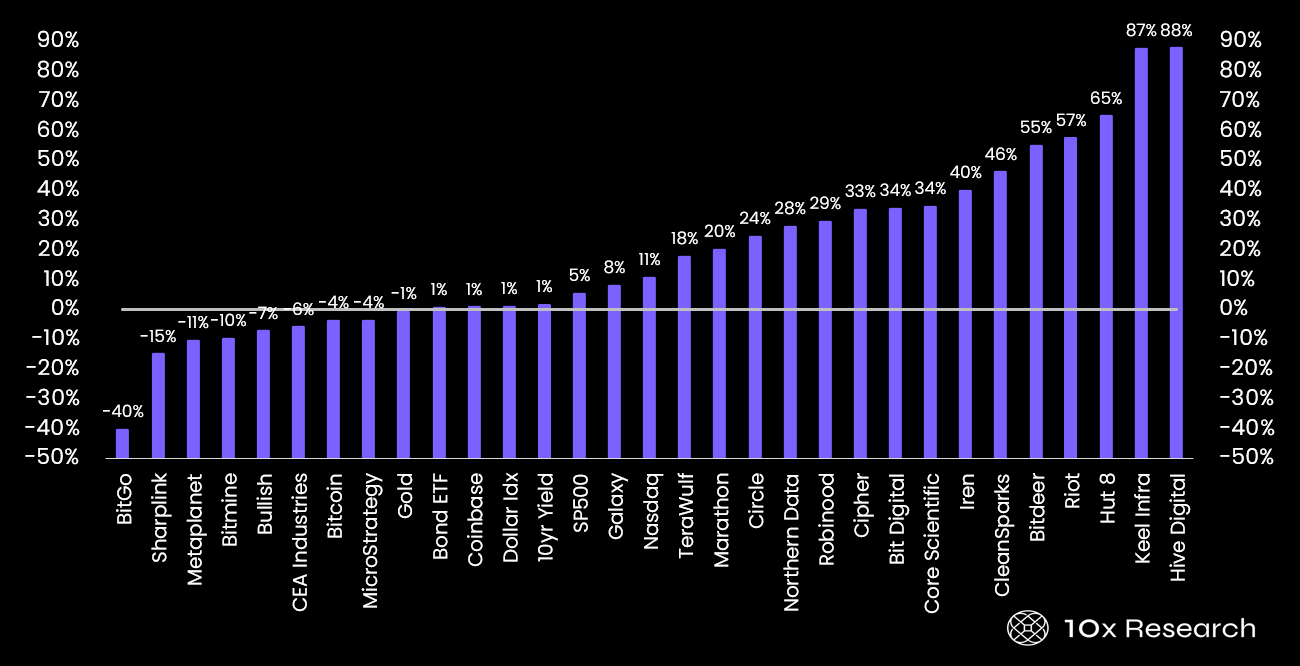

What Actually Happened — Crypto Equities

Bitcoin fell by approximately 3% in May, making the crypto-equity performance chart even more striking. The outperformers had essentially no relationship with the Bitcoin price. Instead, the market rewarded companies that have successfully repositioned their power assets and data center capacity toward AI and HPC workloads. Hive Digital (+88%), Keel Infra (+87%), Hut 8 (+65%), Riot (+57%), Bitdeer (+55%), CleanSparks (+46%), and IREN (+40%) were re-rated as energy and compute infrastructure plays. Their value proposition is now measured in megawatts of deployable capacity and colocation agreements with hyperscalers, not hash rate or block rewards. Core Scientific (+34%) and TeraWulf (+34%), which have been among the most explicit about their AI pivot, delivered for the same reason. The market is effectively pricing these companies as data center infrastructure businesses with a crypto origin story.

Crypto Equity Performance in May

Circle (+28%) and Northern Data (+29%) reflect a separate theme, the broader re-rating of crypto-native financial infrastructure as institutional adoption accelerates and regulatory clarity improves.

The laggards tell an equally coherent story. BitGo (-40%) had no exposure to the AI trade. It is a custody and settlement business whose revenue is tied to trading volumes and assets under custody. Q1 earnings came in well below consensus, with sequential revenue down nearly 40% and adjusted EBITDA swinging to a loss, weighed down by IPO-related costs. A securities investigation announced shortly after the results added further pressure, and multiple analysts cut price targets. At its current price, the stock trades well below its January IPO price, representing one of the more painful post-IPO trajectories in the crypto equity universe.

Metaplanet (-11%) and Sharplink (-15%) are Bitcoin treasury vehicles whose NAV premiums compressed as spot prices softened. The market appears to be repricing the corporate Bitcoin wrapper narrative. Once spot exposure became readily accessible via ETFs, the justification for paying a premium to hold Bitcoin through a corporate structure weakened. MicroStrategy (-4%) showed the same dynamic on a smaller scale, trading roughly flat as the flywheel mechanism has become well understood and is unlikely to generate incremental re-rating without a rising Bitcoin price.

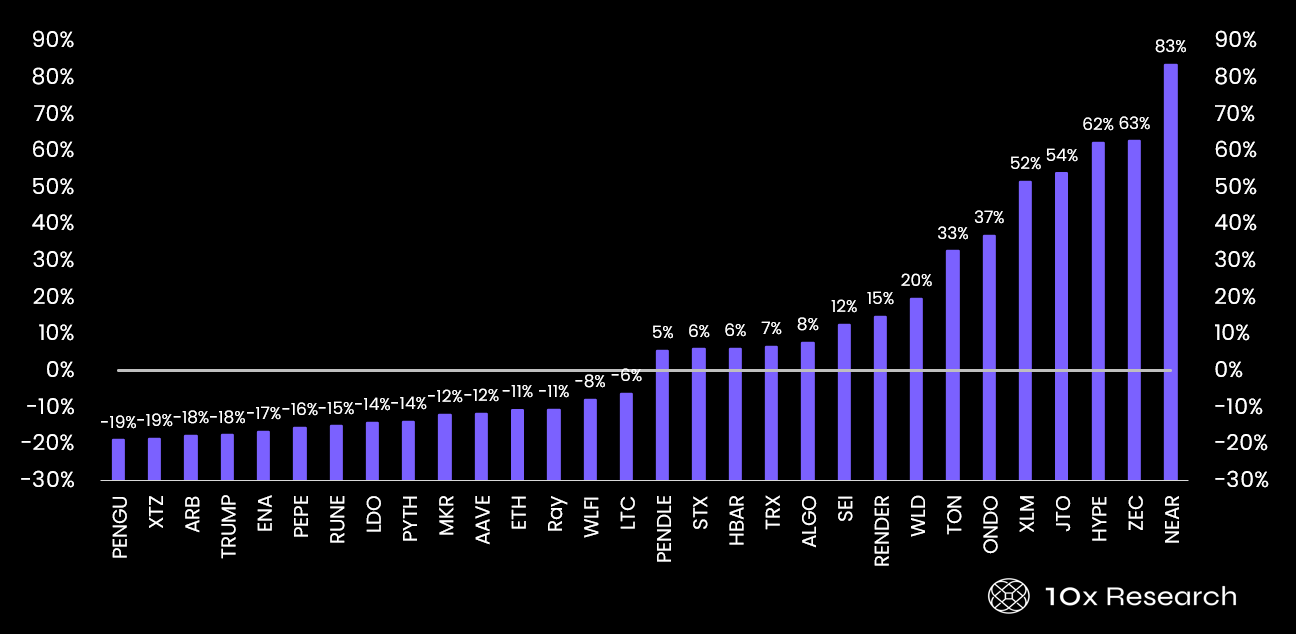

What Actually Happened — Cryptocurrencies

The winning cohort — NEAR (+83%), ZEC (+63%), HYPE (+62%), JTO (+54%), XLM (+52%), ONDO (+37%), and TON (+33%), shared a common thread: genuine utility catalysts or ecosystem-specific momentum rather than speculative narrative drift. NEAR benefited from renewed interest in AI-blockchain integration. HYPE reflected Hyperliquid’s continued dominance in on-chain perpetuals volume, with the protocol generating real fees and attracting sustained institutional attention. ZEC captured privacy token rotation amid dollar-weakness narratives. ONDO and TON represented the two strongest structural themes in crypto beyond Bitcoin, real-world asset tokenization, and a large captive user base converting to on-chain activity, respectively.

Crypto Currency Performance in May

The losing cohort is equally coherent. ETH (-12%), ARB (-18%), AAVE (-12%), and MKR (-12%) all belong to the Ethereum ecosystem, which continued to struggle with a narrative vacuum. Fee burn is declining, L2 cannibalization of base layer activity is real, and institutional allocators have not added ETH alongside their Bitcoin positions in any meaningful way. The ecosystem is technically functional but lacks a near-term re-rating catalyst. ENA (-17%) and PENGU (-19%) represent the two weakest market segments: yield-bearing synthetic stablecoins facing structural questions about sustainability, and pure meme and culture tokens with no durable bid outside speculative cycles. TRUMP (-18%) token has no fundamental support. ARB’s decline reflects the broader L2 dilemma, capturing Ethereum activity without capturing Ethereum valuation.

Survey vs. Reality

Subscribers correctly identified ETH as the most likely underperformer, 35% called it, and it delivered 12% underperformance against a field where many tokens rose sharply. The HYPE conviction also proved accurate, with 40% naming it the top outperform candidate and the token delivering +62%. This was a Long / Short spread of +74% relative performance. Where consensus missed was on the direction of crypto equities: most subscribers expected Bitcoin to roughly keep pace with or outperform MSTR and the miner complex, when in fact the AI infrastructure re-rating drove miners to extraordinary gains entirely disconnected from Bitcoin’s own -3% month.

Participate in the June Survey

Each month, this survey tracks how subscriber conviction evolves alongside market conditions — click here to participate in the June survey.