The Death of the Bitcoin Carry Trade?

Before the Consensus Catches Up

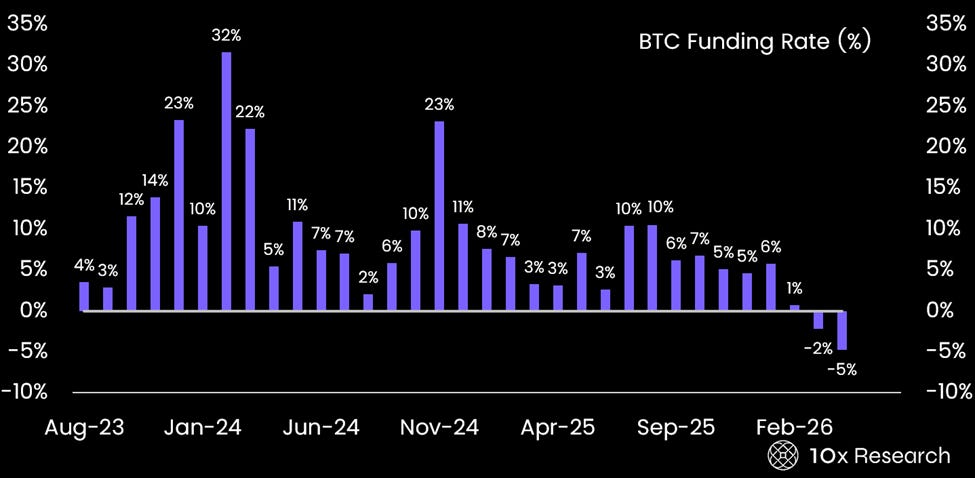

Bitcoin has rallied 15% since early April. Its funding rate has never been more negative when Bitcoin was rallying. That combination has almost no historical precedent. When Bitcoin rises, leveraged longs pile into futures, funding goes positive, and the carry trade pays. The opposite is happening. Short positions are growing into strength.

We have identified three structural sources of this divergence, all tied to accelerating institutional themes. The implications for the basis trade are blunt. The famous carry, long spot, short futures, collect the premium, is not coming back anytime soon. It was a retail leverage phenomenon. Retail has been replaced by institutions that use Bitcoin futures for an entirely different purpose.

The negative funding rate cannot persist indefinitely. But it currently shows how sophisticated players in crypto are positioned, and what they are positioned in has very little to do with a directional view on Bitcoin. The simple cash-and-carry trade has been replaced.

Bitcoin Funding rate (average 30 days rolling, month end)