Circle vs. Coinbase: The Battle for Stablecoin Economics Has Begun

Crypto market intelligence

Why this report matters

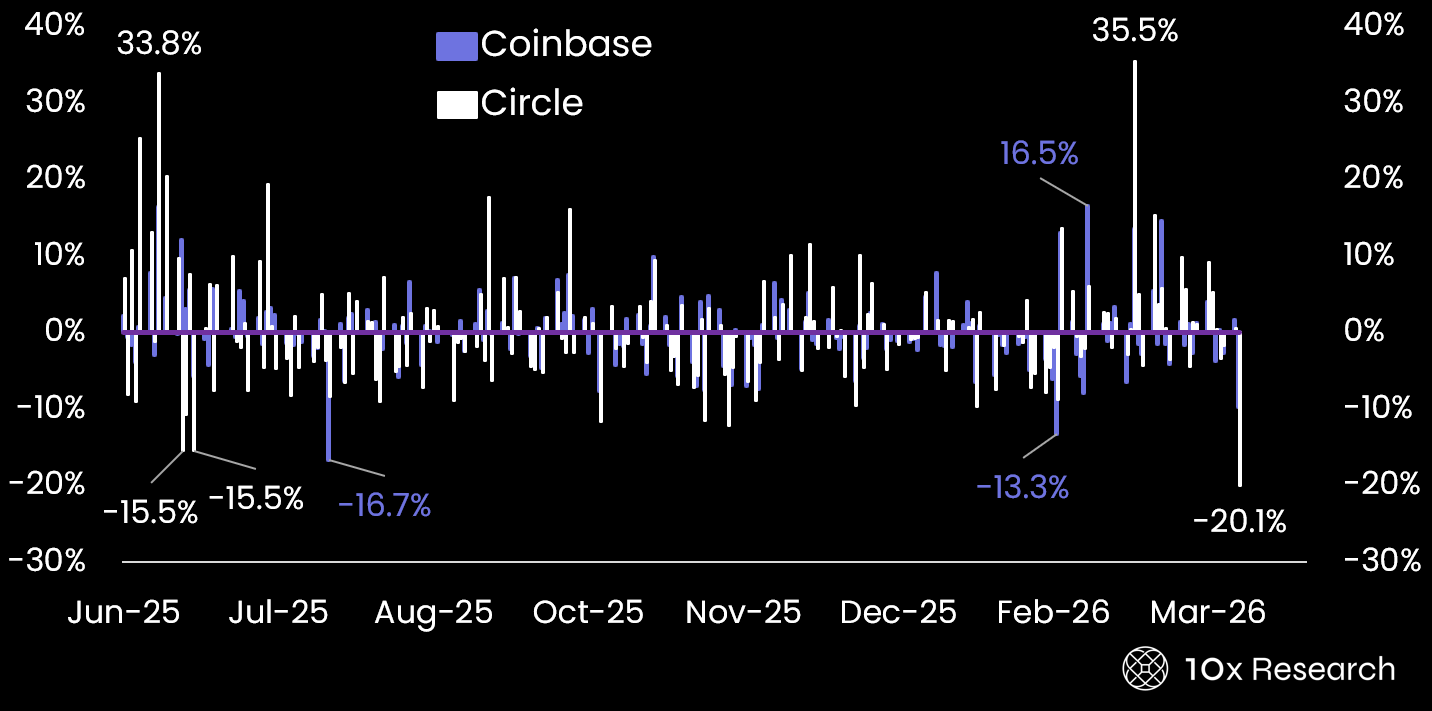

Circle just recorded its largest single-day decline, falling 20%. Some investors are pointing to the CLARITY Act as a growing risk for stablecoin issuers, while others see it as a structural opportunity. In this two-part report (second part will be published later today), we break down both sides of the debate and outline how investors can position accordingly and what it means for DeFi and various crypto currencies.

Coinbase (LHS) vs. Circle (RHS) - Daily change

In our January 18, 2026, report, “Why the Clarity Act Creates a Structural Winner (and a Structural Loser),” we outlined what was at stake for Coinbase and why the bill initially stalled. We argued that Circle supports a federal stablecoin framework because it provides institutional legitimacy to USDC, even if it limits certain short-term “reward” mechanisms. For Circle, regulatory clarity is not a cost but a strategic upgrade, enabling broader institutional adoption, global settlement use cases, and deeper integration with the traditional financial system.

This dynamic places Circle and Coinbase on opposite sides of a classic trade-off. Coinbase’s economics are optimized for near-term earnings through yield-bearing balances, while Circle’s upside is driven by long-term valuation expansion through compliance, scale, and balance sheet credibility. Under a federal regime, Circle may give up part of a highly profitable distribution model, but in return, it gains something more durable: regulatory permanence.

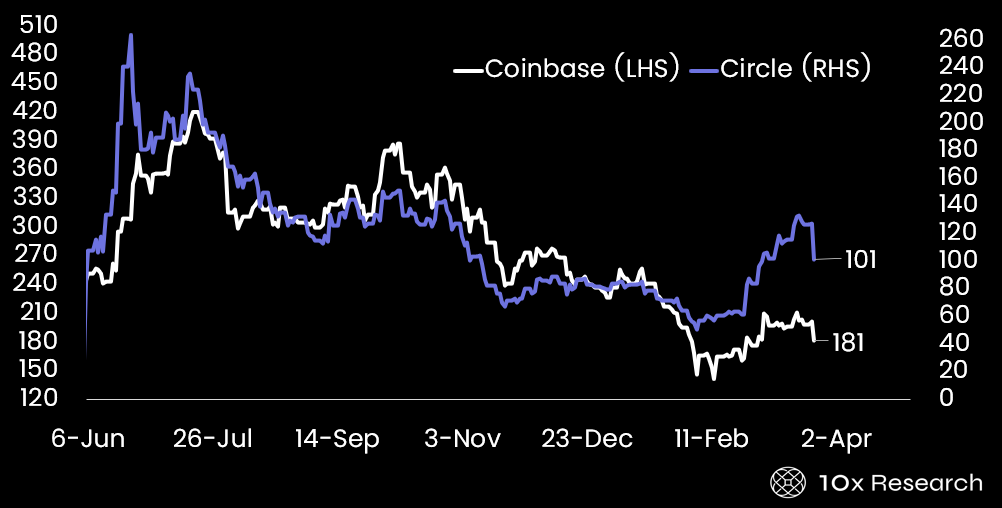

We concluded that this divergence would likely drive relative performance, with Circle positioned to outperform Coinbase. Back then, trading volumes were still subdued, Coinbase had limited fundamental tailwinds, while Circle stood to benefit directly from regulatory clarity and growing institutional demand. Against this backdrop, a long Circle vs. short Coinbase trade remained a compelling relative-value expression. Two months later, and despite a recent ~20% overnight pullback, Circle is still up +29% since our January 18 report, while Coinbase has declined by -25%, reinforcing this thesis.

Circle shares remain up +63% since our February 20 report, where we anticipated that the upcoming earnings release would trigger a short squeeze, which subsequently played out. Another key development (for Circle) we highlighted on February 21 was the launch of the ProShares GENIUS Money Market ETF (IQMM).

As this is a longer research report, we have divided it into two parts. The first revisits our long Circle vs. short Coinbase thesis, assessing whether the trade remains valid and whether current levels present an opportunity to add. We also outline a probability framework around the revenue-sharing agreement, which could materially reshape Circle’s margins and, by extension, its valuation.

Read our arguments and how we would position ourselves around Circle and Coinbase for Part One below, while Part Two examines emerging headwinds for Circle and the broader impact of the CLARITY framework on DeFi, including the opportunities and structural shifts already beginning to unfold.

Coinbase (LHS) vs. Circle (RHS)